2.5M Ontarians lost their family doctor. Shoppers is filling the gap.

TL;DR [show]

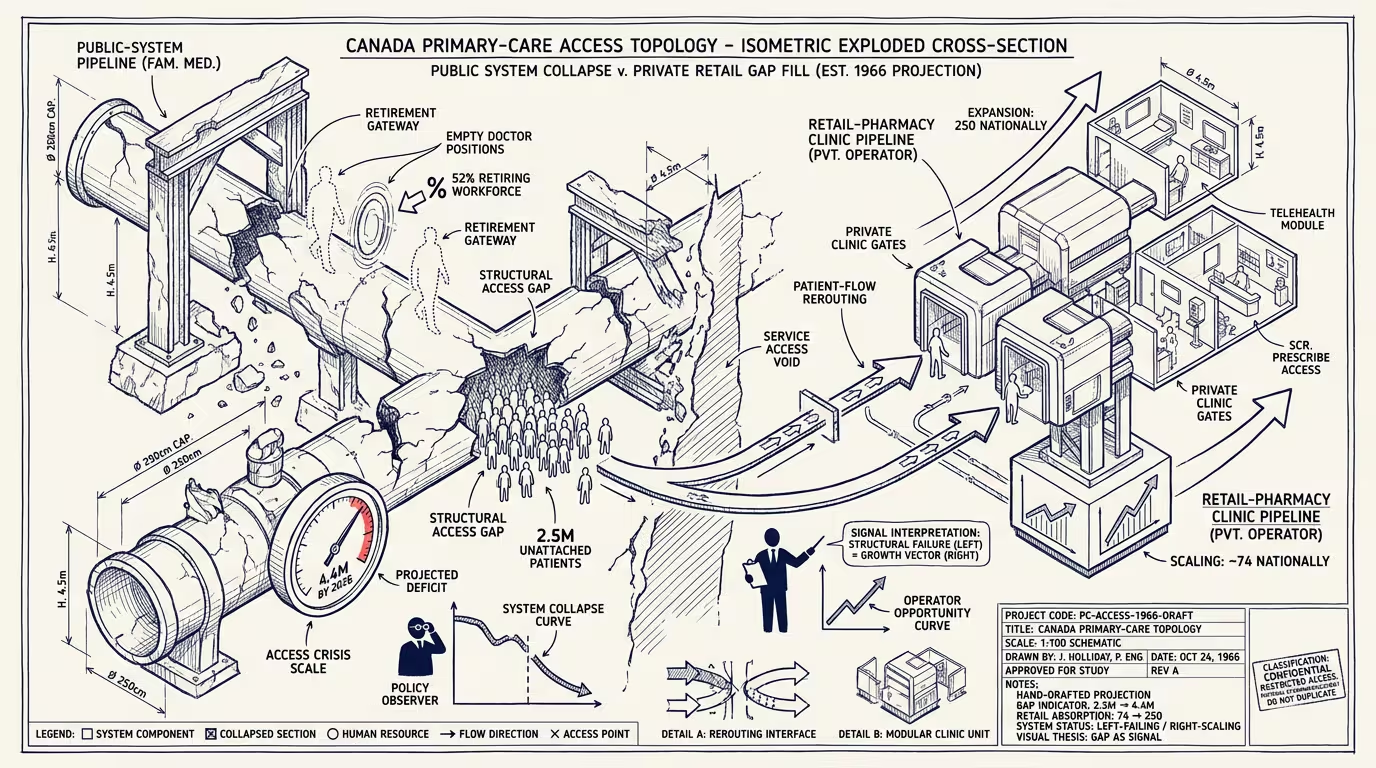

OMA published 2.5M Ontarians without a family physician (projected 4.4M by 2026); 52% of family doctors considering retirement within 5 years; only 26% in team-based care. Loblaw simultaneously disclosed plans to scale Shoppers' pharmacy clinics from ~74 to 250 nationally by 2025. The structural critique and the operator opportunity are the same signal read twice.

The Ontario Medical Association published the numbers in January 2024 and almost no one outside the trade press read them. 2.5 million Ontarians without a family physician. 52% of family doctors considering retirement within the next five years. 26% of patients in team-based care, the model the policy class has been claiming as the future for two decades. By 2026, on the OMA's own projection, 4.4 million Ontarians will be unattached. That is roughly one in three.

Numbers like that have a shape. The shape is structural collapse, not cyclical strain. Cyclical strain has a recovery curve. Structural collapse has a different curve, the one where the institution gets smaller because the people inside it leave faster than the people outside it arrive, and the people who leave do not get replaced.

Family medicine in Ontario is on the structural-collapse curve.

Causes are not mysterious. The compensation gap between family medicine and the procedural specialties is a five-year story that has compounded into a thirty-year career-decision story. New medical school graduates pick their specialty in the year they graduate from medical school; the cohort that picked family medicine in 2014 is the cohort that is leaving family medicine in 2024 because the operating economics of running a family practice did not match what the rest of the medical labor market priced. The team-based-care model the policy class promised in 2008 was supposed to fix this. It did not get funded at scale. The funded version is a small fraction of practices, the OHIP fee structure has not kept pace with operating costs, and the family doctors who could afford to retire are retiring early. The ones who cannot are leaving the province. The ones who cannot leave are running practices that are below operational viability, and they will not be there in 2027.

A cohort of 2.5 million people without primary care is not a dataset. It is a million daily missed encounters with the system that catches early disease, the system that titrates a chronic medication before it becomes a hospitalization, the system that knows the patient's mother had the same thing. None of those happen at a walk-in clinic. None of them happen in an ER. The cost of not having them shows up later, in an emergency department visit that should have been a clinic appointment six months earlier, and the cost gets paid by a population that, by every cohort analysis the literature offers, is already disproportionately the population the public system was designed to protect.

Public system is not going to fill the gap. That claim is contestable but the contest is largely among people who do not have a plan. The plan everyone has is more residency seats, faster credentialing for foreign-trained physicians, and incentive funding for team-based clinics. All three are correct. None of them produce a primary-care doctor inside the next four years, which is the time horizon over which the gap doubles.

What is filling the gap is, by January 2024, visible.

Loblaw — the parent company of Shoppers Drug Mart — announced in late January that the pharmacy chain will operate 250 pharmacy care clinics nationally by end of 2025, scaling from approximately 74 at announcement. The Alberta plan alone targets 103 clinics, three times the original target. The clinics treat colds, urinary tract infections, pink eye, several chronic-disease management protocols, and a growing list of conditions that provincial regulators have authorized pharmacists to manage. Provincial billing covers most of the visit cost. The patient walks in. The encounter is fifteen to twenty minutes. The follow-up, when needed, is at the same clinic.

A private retailer is filling the access gap left by the public primary-care system.

Both readings are visible by January 2024. Structural critique writes itself: the public primary-care system has failed at the thing public primary-care systems exist to do, and the gap is being filled by a publicly-traded grocery chain that has the capital to deploy 250 clinics at scale and the regulatory relationship to bill the province for the visits. Operator opportunity writes itself: the largest captive primary-care expansion in Canada in 2024 is happening inside a retail chain, the unit economics work because foot traffic is already there, the labor model works because pharmacists were already being underutilized, and the funding model works because the province pays per-visit at a rate the chain can absorb at the volume it operates.

Both readings are correct. The trade press treats them as distinct stories because the trade press assumes structural critique and operator opportunity live on different desks. They do not live on different desks. They are the same desk, two-thirds of the way through one of the biggest healthcare-delivery substitutions Canadian primary care will see this decade.

The operating model is worth dwelling on because it is not a retail model rebranded as healthcare. The Shoppers clinic format inherits from pharmacy operations: clinic hours map to pharmacy hours, clinical staff sit inside or adjacent to the dispensing counter, the inventory and labor are shared across the retail footprint, and the patient is already a Shoppers customer for adjacent products before they are a Shoppers patient. Customer-acquisition cost is, in retail terms, near-zero. The marginal cost of adding a clinic visit to an existing pharmacy footprint is, by every operator analysis, substantially below the cost of standing up a new community-health-clinic location. The province pays the same rate. The chain absorbs the difference.

That is, of course, the operating model that family-doctor offices used to run, before the operating economics broke. The pharmacy chain is running a version of community medicine that is a small specialization of a larger retail business. The family-doctor's office is running a version of community medicine where the retail business is the medicine, and the medicine is below operational viability under the current fee structure. The structural difference between the two operating models is that one is solvent and one is not.

There is a version of this story where the policy class tries to defend the family-doctor's office as the right operating model, on the principle that the doctor-patient relationship is the load-bearing primitive and the pharmacy chain cannot replicate it. That argument is correct and, in the current operating-economics environment, irrelevant. A 2.5-million-Ontarian access gap does not get filled by an operating model that requires fee-structure reform to become solvent. It gets filled by an operating model that is already solvent.

What this means for the next decade is structurally legible. Provincial regulators will continue to expand the pharmacist scope-of-practice. The pharmacy chains will continue to expand the clinic footprint. The OHIP fee structure will continue to lag. Family practices will continue to close. The cohort of patients who used to have a family doctor will continue to migrate to pharmacy clinics for routine care, to walk-in clinics for acute care, to ERs when neither is available, and to the public system at the moments where the disease has progressed past the point a family doctor would have caught it. The cost will be paid by a cohort that will not show up in a single news cycle. It will show up in five-year mortality differentials and in chronic-disease trajectories, and the policy class will, at some point, decide that the cohort cost is more than the cost of fee-structure reform, and family medicine will, ten years from now, be in a different operating-economics position. Or it will not. The cohort is waiting either way.

The part that holds is that the next decade of Canadian primary care will be co-delivered by a public-system whose family-medicine layer is structurally thinning and a private-system whose pharmacy-clinic layer is structurally thickening, and the line between them will get blurry the way the line between independent bookstore and Amazon got blurry, and the discourse will lag the operating reality by about five years. That is roughly the lag the public discourse has on most healthcare-delivery substitutions, of course.

—TJ