The 2025 digital health vintage looks like a real industry. The 2021 vintage wore a stethoscope.

TL;DR [show]

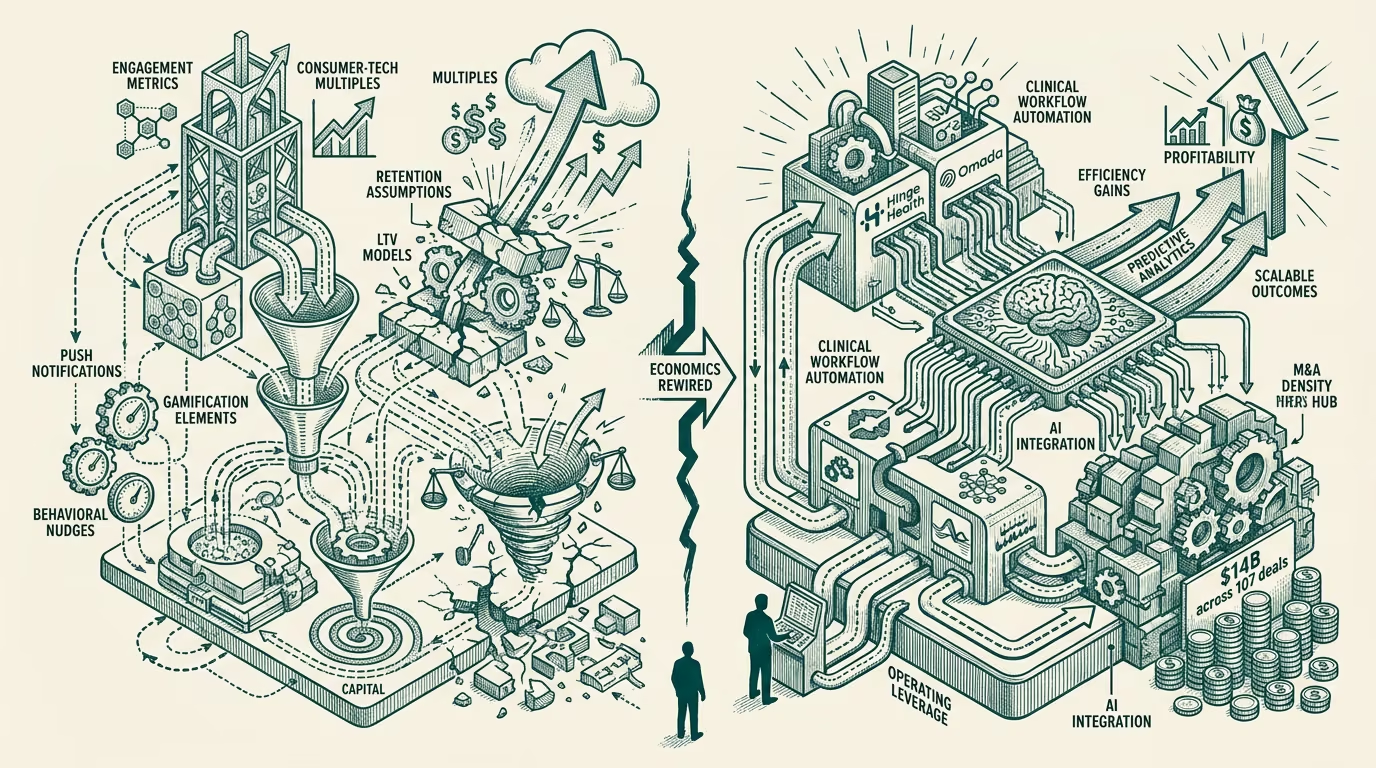

The 2025 digital-health vintage, with approximately $14B raised, Hinge Health and Omada among the visible IPOs, and roughly 107 M&A deals through the year, looks structurally different from the 2021 vintage. The 2025 cohort wins on operating leverage and AI integration; the 2021 cohort won on engagement metrics that did not translate into durable economics. Medium retrospective comparing the two vintages, naming what broke between them, and what the structural difference implies for the 2026-2028 cohort.

The 2025 digital-health vintage, with approximately $14 billion raised across roughly 280 funding rounds, the Hinge Health and Omada IPOs as the visible public-markets exits, and roughly 107 M&A deals consolidating the broader category, looks structurally different from the 2021 vintage that produced the prior cycle's operator-class energy. The 2025 cohort wins on operating leverage and AI integration. The 2021 cohort won on engagement metrics that did not translate into durable economics. The two vintages share the digital-health label and not much else.

This essay walks the comparison. The 2021 vintage profile, what broke between 2021 and 2025, the 2025 vintage profile, what is structurally different, and what the structural difference implies for the 2026-2028 cohort.

The 2021 vintage profile

The 2021 digital-health vintage was the visible peak of a multi-year consumer-tech-meets-healthcare investment thesis. The total category capital raised in 2021 ran approximately $29 billion, with the funding heavily concentrated in consumer-facing applications, telehealth-as-a-feature platforms, mental-health subscription services, and the broader category of products that took consumer-tech engagement-and-retention frameworks and applied them to healthcare.

The valuation discipline through 2021 priced these companies against consumer-tech multiples (high revenue multiples, generous treatment of growth-stage unit economics, optimistic assumptions about retention-and-LTV trajectories). The implicit thesis was that healthcare consumers would behave like consumer-tech consumers, with engagement-driven retention producing the long-term LTV the unit economics required.

The thesis was substantially wrong. Healthcare consumers did not behave like consumer-tech consumers. The retention curves dropped faster than the unit economics required. The reimbursement-and-buyer relationships that healthcare actually runs on were not built into the consumer-tech-style products. The clinical-and-regulatory complexity that healthcare carries was treated as friction to design around rather than as the structural reality of the operating environment.

By 2022-2023 the trajectory had become visible. The 2021 vintage was over-funded, structurally fragile, and on track for substantial mortality. The mortality landed through 2022-2024.

What broke between 2021 and 2025

Three things broke meaningfully through the 2022-2024 period.

The consumer-tech-engagement framework broke as a thesis. Companies that had built their unit economics around engagement-driven retention found that the engagement did not translate into the long-term retention the LTV required. The retention curves looked good for the first 6-12 months and then degraded faster than the consumer-tech analog had implied. By 2023 the venture-class had stopped pricing healthcare-startups against consumer-tech multiples without strong demonstration that the retention was durable.

The reimbursement-and-buyer-relationship side became central. The companies that survived through 2022-2024 were the ones that had built durable employer-and-payer-and-provider relationships, which produced revenue that did not depend on consumer engagement alone. The companies that had built only consumer-facing direct-to-consumer subscription models faced the consumer-acquisition-and-retention challenge with no fallback channel.

The clinical-and-regulatory infrastructure became a moat rather than a friction. Companies that invested heavily in clinical-validation, regulatory-compliance, and the broader operational infrastructure that healthcare requires built defensible positions. Companies that treated this work as overhead struggled.

The 2025 vintage profile

The 2025 vintage emerges from the 2022-2024 cull as a smaller, more disciplined, and more structurally durable category. The roughly $14 billion raised in 2025 is materially less than 2021 in absolute terms but is concentrated in companies with clearer unit economics, more sophisticated buyer-relationship strategies, and meaningful AI integration that the 2021 vintage could not have built.

The Hinge Health IPO in mid-2025 is a reasonable exemplar. The company built employer-channel revenue rather than direct-to-consumer subscription revenue. The product runs against musculoskeletal-pain populations with measurable clinical outcomes that the employer-buyer cares about. The unit economics are bounded by the employer-procurement relationship rather than by consumer-acquisition costs. The exit pricing reflected enterprise-software multiples rather than consumer-tech multiples.

Omada's exit in 2025 ran a similar shape. Hims, the publicly-traded telehealth company, has continued to grow its revenue and reach profitability through the same period, with its model running on a hybrid consumer-and-prescription-fulfillment basis that produced durable economics. The 2025 cohort is broadly running this hybrid pattern: consumer-facing where the consumer-relationship is genuinely durable, channel-and-buyer-relationship where it is not, and clinical-or-regulatory infrastructure that defends against the EHR-eats-the-feature pattern discussed elsewhere.

What is structurally different

The structural differences between the 2021 and 2025 vintages run along three axes.

The first axis is the buyer-and-channel sophistication. The 2025 cohort is built for the actual healthcare-buyer-class (employers, payers, health systems, pharmacy partners) rather than the consumer-tech-buyer fantasy. The 2025 sales-and-deployment cycle reflects the actual healthcare-procurement reality. The 2025 unit economics reflect the actual reimbursement-and-pricing structure that healthcare runs on.

The second axis is the AI integration. The 2025 cohort is built with AI as a core capability rather than as a marketing-class add-on. The 2025 products use AI for clinical-decision support, workflow-and-coordination automation, patient-facing communication-and-engagement, and operational-back-office work. The 2025 cohort's unit economics are meaningfully better than the 2021 cohort's because the AI integration has compressed the operating costs in specific categories that the 2021 cohort had to staff humans for.

The third axis is the operating-leverage discipline. The 2025 cohort is operating with leaner headcount, more disciplined unit economics, and clearer paths to profitability than the 2021 cohort. The 2025 leadership-class includes substantial healthcare-operating experience that the 2021 cohort sometimes lacked. The 2025 boards include investors and operators who have lived through the 2022-2024 cull and have calibrated their advice accordingly.

What this implies for the 2026-2028 cohort

The part that holds for operators and investors evaluating the 2026-2028 digital-health cohort is that the 2025 vintage represents the recalibrated baseline. Companies that build to the 2025 standard (real buyer-and-channel work, real AI integration, real operating-leverage discipline) will be priced and supported accordingly. Companies that try to recreate the 2021 model (engagement-driven consumer-tech in healthcare) will face the structural problems the 2022-2024 cull exposed and will not get the patient-class capital that absorbed the 2021 mortality.

The category is not in retreat. The category is in the post-cull recalibration phase, with the 2025 vintage demonstrating what the recalibrated model looks like. The 2026-2028 cohort will continue to consolidate, with M&A activity likely to remain elevated as the platform-tier vendors (Salesforce Health Cloud, Microsoft, Epic, the major payers and providers) absorb the specialty-tier startups and as the specialty-tier consolidates among itself.

The 2025 digital-health vintage looks like a real industry because it is built to the actual operating environment of the healthcare category, not the consumer-tech analog the 2021 vintage was priced against. The 2021 vintage was consumer tech wearing a stethoscope. The 2025 vintage is a healthcare technology category that has, finally, learned to operate as the healthcare technology category it always needed to be. The recalibration was expensive. The result is more durable than the 2021 vintage was. The next several years will continue to compound on the 2025 baseline.

—TJ