The Agentic Reckoning Comes for Travel

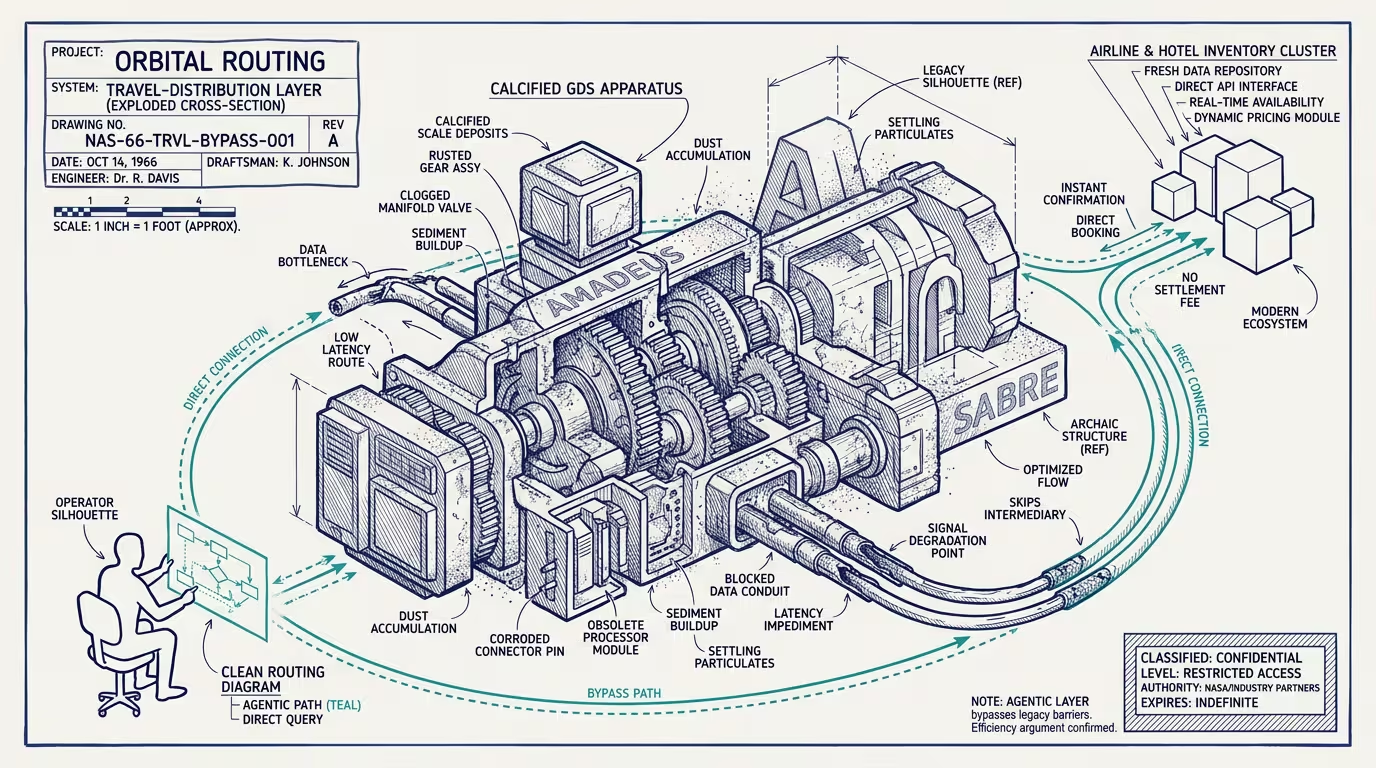

The last time I sat inside a GDS terminal — properly inside one, not a wrapper, not an API call, not an abstraction layer three handshakes away from the Amadeus or Sabre rails — was sometime around 2015. I was walking a product team through why booking-flow latency at the millisecond level correlated, statistically, with abandonment rates. The GDS was indifferent to this. It had always been indifferent to this. That is what monopoly infrastructure does: it stops caring about the thing the customer is actually trying to do.

I have spent a meaningful chunk of my career inside the global travel stack, at platforms that moved hundreds of millions of dollars in gross bookings, across 25 markets, at revenue trajectories that required you to actually understand how the machine worked rather than just what it returned. I am not a travel journalist. I am someone who spent years looking at the same intermediary layer most people only see as a booking confirmation email.

That layer is dying. Not quickly, not cleanly, and not all at once — but dying in the way that large infrastructure always dies: slower than the critics say, faster than the incumbents believe, and almost always for a reason the incumbents had the data to see and either didn't, or chose not to act on (people like to hold onto their jobs; status quo protects them, until it doesn't).

< strong>Here is the thesis, as plainly as I can put it:</strong> the agentic AI shift will kill or permanently diminish the intermediary categories that exist primarily to aggregate and sort information for a human decision-maker. It will spare, or strengthen, the categories that own genuine infrastructure, real relationships, or proprietary data that an AI agent can't easily replace or route around. The sorting is already underway. By 2028, it will be legible to anyone who bothers to look.

---

What metasearch was actually for

Kayak launched in 2004. Google Flights became a real product around 2011. By the mid-2010s, metasearch had matured into a specific and genuinely useful thing. It was a neutral aggregation layer that let a human traveler compare options across OTAs and suppliers without visiting fifteen different tabs. The UX was built around search as the primary verb. You had a question ("what does it cost to get from Toronto to London on these dates?") and the metasearch product answered it by doing the tab-hopping on your behalf.

That was a real problem. It is no longer the bottleneck.

When the query interface is a language model rather than a search bar, the aggregation layer that metasearch provided becomes a function that the LLM performs as part of reasoning, not a destination the user navigates to. This is not a speculative development. Perplexity is already answering "what's the cheapest way to get to Lisbon in October" with synthesized comparisons that never touch a metasearch URL. ChatGPT's browse capability does the same. The agentic travel planners now in preview at several of the major AI labs will, within 18 months, execute the comparison and the booking in a single loop without surfacing the metasearch layer to the user at all.

Kayak is aware of this. Google Flights is, by definition, a feature inside the organization best positioned to either solve this problem or become it. The independent metasearch players (and there are more of them than the casual observer tracks) are in a harder position. The UX they were built for is not the UX the next cohort of travelers will default to.

< strong>Prediction, with a window:</strong> by the end of 2027, one or two major independent metasearch properties will have either been acquired (likely by an OTA looking to consolidate demand) or will have pivoted their product positioning substantially away from the consumer comparison interface. The ones that survive will do so by becoming infrastructure: API-first, white-labeled into the AI interfaces rather than trying to remain the destination.

---

The OTA question is more complicated, and that's the interesting part

Booking Holdings and Expedia Group are not going to disappear. That's the wrong question. The right question is: what do they become?

Both companies have spent the last decade building enormous supplier relationship networks, inventory contracts, and the payment and trust rails that make a booking legally and financially real. Those things are not trivial to replicate. An AI agent that wants to book a hotel in Amsterdam does not need Booking.com's interface, but it does, for now, need something like Booking.com's supplier relationships, fraud infrastructure, and dispute resolution capability to actually deliver a confirmed reservation with recourse.

The scenario I find most plausible, and the one the OTAs would be wise to accelerate toward deliberately: they become the commodity backend for AI-mediated booking, the way AWS became the commodity backend for internet services. The brand-to-consumer relationship attenuates or disappears entirely. What's left is a B2B infrastructure business (inventory access, payment rails, contract fulfilment) that the AI agents route through without the user ever knowing the name of the company that made the booking possible.

This is a legitimate business. It is not the business either company is currently optimizing for, staffed for, or priced for. The margin compression that accompanies this transition will be significant.

< strong>The alternative scenario, the one both companies are actively betting on, is that brand loyalty survives the agentic shift.</strong> That travelers will explicitly instruct their AI agents to "book through Booking" the way they might say "get me an Uber, not a Lyft." I think this is possible for a narrow segment: frequent travelers with strong loyalty program attachments, corporate travelers whose expense systems specify suppliers, and a set of older users who don't fully trust the agent. It is not the dominant trajectory for new traveler cohorts coming up on AI-native interfaces.

< strong>Prediction:</strong> by 2026, one major OTA will have a meaningful API product explicitly designed for AI agent access, distinct from its consumer-facing booking flows. The company that moves first and prices it aggressively will capture a disproportionate share of agentic booking volume. The company that treats it as defensive and secondary will spend 2029 explaining to investors why its brand consumer business is declining faster than the API business is growing.

---

The GDS question, answered honestly

Amadeus, Sabre, Travelport: these are the rails. They power a significant fraction of global airline ticketing, and they have survived longer than almost anyone predicted they would because the airline industry's own booking infrastructure is so deeply entangled with them that switching costs approach prohibitive.

I have opinions about this that I formed in rooms where the GDS reps were also sitting, and the honest version is this. The rails will survive longer than the consumer-facing intermediaries, and they will survive not because they have innovated but because the thing they do (manage the inventory, pricing, and ticketing agreements that make a boarding pass real) is genuinely difficult to replicate on a compressed timeline.

What will erode is their pricing power. NDC (New Distribution Capability, the IATA standard that lets airlines sell directly without the GDS content abstraction layer) has been "about to change everything" for the better part of a decade and has changed things more slowly than advertised. But the AI-mediated booking shift creates a new vector. If AI agents start booking meaningfully more volume through direct airline APIs rather than GDS-aggregated content, the GDS transaction fee model starts to compress in ways that are harder to manage than the NDC transition was.

The travel executives I respect in this space are thinking about the GDS as a five-to-ten year managed decline rather than an immediate disruption. That framing is probably right. "Managed decline" is still decline.

< strong>The category that's most durable, least glamorous:</strong> corporate travel. TMCs, the travel management companies that handle corporate accounts, are the intermediary category I'd bet on last. Not because they've figured out the agentic shift (most haven't), but because their value proposition is fundamentally about policy compliance, duty of care, consolidated billing, and the legal requirement to know where your employees are when something goes wrong. An AI agent can optimize a corporate trip's routing; it cannot sign the agreement that makes the company's CFO comfortable that the booking is auditable.

The TMC that builds native AI agent interfaces into corporate travel policy management, that makes the compliance layer the product rather than a constraint on the booking layer, has a real business in the agentic era. The ones that don't will find that their accounts increasingly go directly to OTA API products and self-manage.

---

Three things I expect to be able to point back to by 2028

One: the consumer metasearch interface, as a standalone destination, will have shrunk to a fraction of its current traffic volume. The aggregation function will have been absorbed into AI interfaces. The metasearch brands that survive will be B2B.

Two: at least one major OTA will have made a substantial organizational and product bet on becoming AI-infrastructure-first rather than brand-consumer-first. The market will initially undervalue this, then overvalue it, then settle.

Three: airline loyalty programs, the one intermediary category I haven't addressed in detail, will prove more durable than almost any other. The reason is simple. Loyalty programs are not information aggregators. They are customer data assets and relationship anchors that create switching costs at the individual level. An AI agent can book the cheapest fare; it cannot tell a traveler that they're 8,000 points from status, and that status gets them the upgrade that makes their monthly Toronto-to-London commute survivable. That information asymmetry is the moat. It is a smaller moat than it used to be, and loyalty programs are already seeing that AI tools can surface it more cheaply than the airlines' own apps do. But it's a real moat, and it will last longer than most of the others. Until, inevitably, someone builds an LLM specialized in and trained on airline loyalty data and programs, or rebuilds one that exists today to work with leading LLMs.

I helped scale this industry. I watched, specifically, how it looked when a new distribution layer came in and the incumbents had three options: adopt early, adopt late, or wait to be routed around. The ones who waited to be routed around eventually showed up in a post like this one.

The machine is a participant now. The intermediaries who figured out their own role in that equation in the last two years will be fine. The ones still waiting for clarity, on NDC, on direct booking, on the agentic channel, are writing the next chapter of this piece for me.

I watch this industry the way you watch a place you loved that's changing faster than the people who live there can see. Some of what's dying deserved to die. Some of it didn't.

—TJ