AI's capital gravity is pulling investment away from every adjacent tech sector.

TL;DR [show]

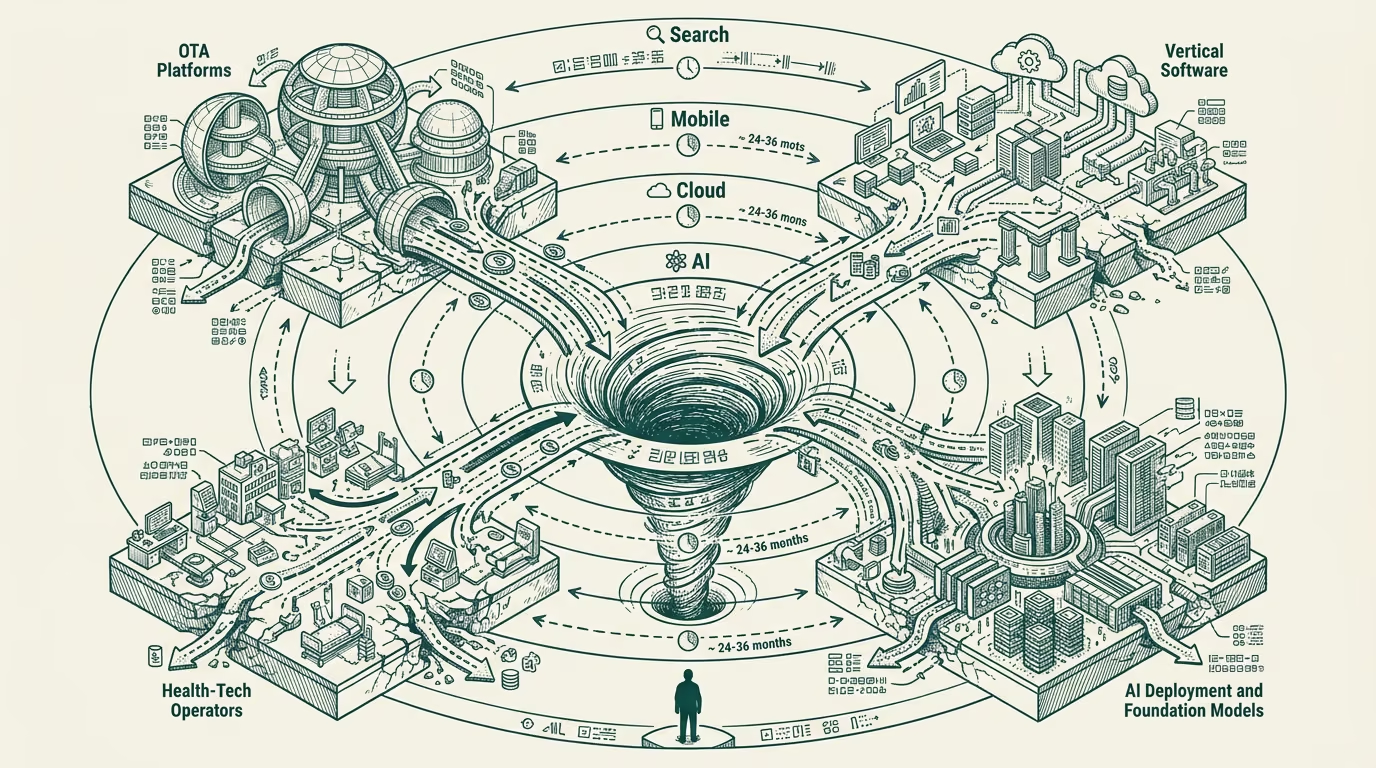

OpenAI's $6.6 billion raise at $157 billion valuation in October 2024 is the visible signal of the AI capital-gravity shift that has been reshaping investment allocation across the broader tech category through 2024. The pattern is the fourth capital-gravity event of the past two-and-a-half decades (search in the late 1990s, mobile in the 2010s, cloud through the 2010s-into-2020s, AI now). The historical pattern is that adjacent tech sectors that do not integrate the gravity-event capability quickly enough get starved of investment, with the consequence being a 24-36 month survival window for category-class operators.

OpenAI's $6.6 billion raise at $157 billion valuation in October 2024 is the visible signal of the AI capital-gravity shift that has been reshaping investment allocation across the broader tech category through 2024. The raise is one of multiple capital-class events that have concentrated investment toward the foundation-model and AI-deployment categories, with the cumulative effect being that adjacent tech sectors are seeing measurable contraction in available capital, available talent, and available investor attention.

The pattern is the fourth capital-gravity event of the past two-and-a-half decades. Search consolidated capital in the late 1990s and into the 2000s, with the operator-class learning that investment in adjacent categories that did not integrate search-class capabilities was structurally starved. Mobile consolidated capital through the 2010s, with the same dynamic at the broader tech category level. Cloud consolidated capital through the 2010s and into the 2020s, with similar consequences. AI is the fourth event, and the historical pattern suggests the same shape will produce the same consequences in the adjacent categories.

For operator-tier buyers in the adjacent categories (OTA-class, health-tech-class, broader vertical-software-class), the historical pattern produces a roughly 24-36 month survival window. Companies that integrate the gravity-event capability into their operating model and product within that window survive and continue to attract investment. Companies that do not integrate within the window face capital-class consequences (lower valuations, harder fundraising cycles, talent migration to the gravity-event category, longer sales cycles as buyers attend to the new-capability category) that compound through the subsequent years.

The current cycle is producing the same shape. OTAs that have integrated AI into the booking-funnel and disruption-management workflows are receiving better capital-class treatment than OTAs that have not. Health-tech companies that have integrated AI into the clinical-decision-support and operational-workflow categories are similarly differentially treated. Vertical-software companies in adjacent categories (legal-tech, financial-services-tech, government-tech) are running the same pattern, with the operators who integrate quickly receiving differential capital-class treatment.

The implication for the operator is that the integration window is real and the timeline is short. Operators who plan against the assumption that the AI-integration work can be deferred for several years are running against the historical pattern, with the consequences being predictable from the prior three capital-gravity events. The integration work is hard, the talent acquisition is competitive, the product redesign is meaningful, and the timeline is compressed. The operators who absorb the cost of the integration work within the window survive the gravity-event with their capital-class position intact. The operators who do not absorb the cost face the structural consequences.

For the trade-press and the broader investor-class commentary, the pattern is well-documented in the historical record. The current AI-gravity event is producing the same shape, and the trade-press coverage that does not surface the integration-window framing is missing the operationally-relevant signal.

Operators reading the OpenAI raise and the broader pattern of AI-class capital concentration should be allocating substantial portions of their 2025 strategic-planning capacity to the AI-integration work. The window is open. The window is closing. The historical pattern is clear about what happens to operators who do not act inside it. Build accordingly.

—TJ