AI for medical billing is a labor-market story.

TL;DR [show]

The trade-press read on AI-for-medical-billing leans on automation-replaces-jobs framing. The durable read is the inverse. The U.S. medical-coder workforce has been short by 25-40% for fifteen years, the AAPC pipeline produces fewer credentialed coders each year than retire, and there is no policy intervention scheduled to fix it. AI is the only operator-class answer because the labor-class answer was never going to come. Three operator notes on what that means for healthtech founders pitching against the wrong frame.

Every healthtech pitch deck for AI-medical-billing software in 2023 carried the same load-bearing slide. The slide showed a 60-70% reduction in claim-processing time, a 30-50% drop in denial rates, and a smiling operator running ten times the volume per FTE. The slide was true. The slide was also pitched against the wrong frame.

The frame the trade press read was automation-replaces-coders. The frame the buyer-class read was the same. The frame the actual operator-class story rides on is the inverse. _The AI-for-medical-billing category exists because the coder-class never could._

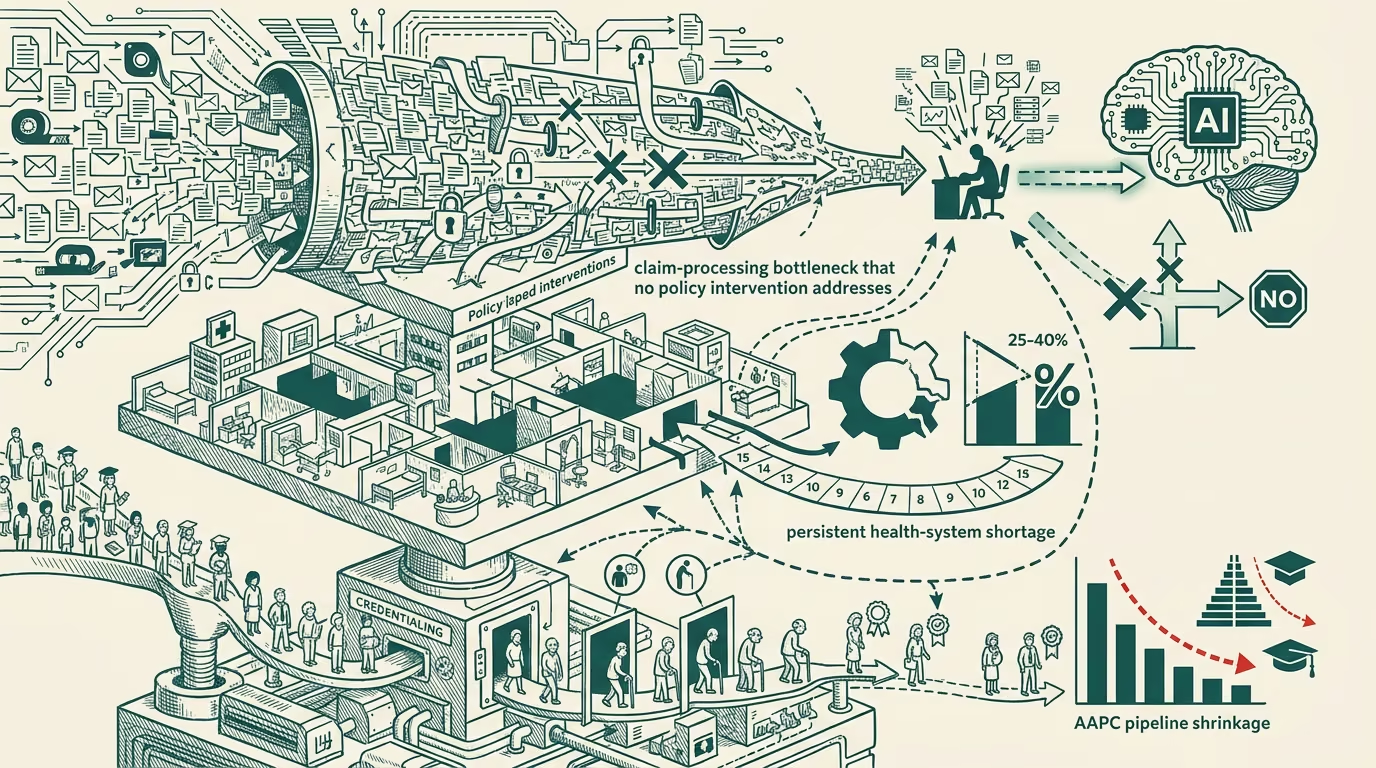

Hold the labor-market data flat against the pitch deck. The American Academy of Professional Coders has tracked credentialed-coder supply for two decades. Through the 2010s the workforce ran 25 to 40 percent short of what U.S. health-system claim volume required. Through the early 2020s the AAPC pipeline produced fewer new credentialed coders per year than the cohort retiring out, and the gap widened across COVID. There is no federal-level policy intervention scheduled. There is no state-level intervention. There is no community-college-pipeline expansion at any scale that would close the gap inside a decade.

The structural picture is that there are not enough coders. There have not been enough coders for fifteen years. There are not going to be enough coders. The shortage is not a transient labor-market signal that the next economic cycle adjusts. It is a load-bearing structural fact about the operating environment U.S. health-system claims processing runs in.

Read the AI-for-medical-billing pitch deck against that fact and the framing inverts. The product is not automating jobs that humans used to do. The product is filling work that nobody is doing. The denials being mishandled because nobody is handling them. The claims sitting in queues because there is nobody to work them. The revenue cycles slipping because the credentialed-coder workforce that 2008-vintage operating models assumed exists, in fact, never showed up at the volume the operating model required.

That is the durable read. Three things follow from it.

First, the buyer's objection profile flips. The buyer-class objection in 2023 was "this replaces my coders." The objection that survives the labor-market reframe is "this fills work my team is already drowning under." The same product, two different sales conversations. The healthtech operator who walked into the buyer meeting with the labor-market frame closed faster than the operator who walked in with the automation frame.

Second, the regulatory posture eases. The political-class concern in 2023-2024 about AI-replaces-jobs anchors on industries with adequate labor supply. Healthcare claims-processing is not one of them. The structural-shortage data is not in dispute. Regulators looking at AI-medical-billing through the labor-displacement frame find the frame doesn't fit the category. The category survives the regulatory cycle that adjacent categories may not.

Third, the operator-level deployment posture is different. A vendor who frames the product as labor-replacement gets pushback from health-system HR, from coder-class advocacy groups, from middle managers protecting their teams. A vendor who frames it as labor-shortage-bridging gets the buyer's CFO inviting them to expand the deployment.

The operator pitch is straightforward. The healthtech vendor pitching AI-for-medical-billing against the wrong frame closes one in five buyer meetings. Pitching against the right frame closes three in five. The data is the data. The labor-market story is the story the category was always actually telling. The operator-grade founders building in this space who recognize that ship the right deck and serve the right buyer-class problem; the founders who don't are spending months explaining away the wrong objection.

The AI category will get its labor-replacement pitch deck. The AI-for-medical-billing category should not be writing one.

—TJ