The AI-generated travel itinerary product was always going to be the booking funnel. Expedia's 10-K confirmed it.

TL;DR [show]

The wave of AI-generated travel itinerary products that ran through 2023-2024 mostly faded by 2025, with the surviving products having repositioned away from the standalone-itinerary-generation framing they launched against. The structural reason was visible from the start: itinerary generation is the wrong unit of work for an agent because the customer's actual want is the bookable-fulfillment, not the itinerary draft. Expedia's 10-K disclosure language through 2024-2025 confirms the read by acknowledging that the company's AI investment landed on booking-funnel optimization rather than standalone itinerary-generation. Medium case-study walking the wave, the structural mismatch, the Expedia confirmation, and what the next category of AI-travel products needs to internalize.

The wave of AI-generated travel itinerary products that ran through 2023-2024 (Mindtrip, Layla, Vacay, Wanderboat, GuideGeek, plus the various brand-tier offerings from major OTAs and chains) mostly faded by 2025. Some companies wound down. Some were absorbed into broader products. Some repositioned aggressively away from the standalone-itinerary-generation framing they had launched against. The visible category survival rate, two years post the early-2024 peak, is meaningfully lower than the venture-class consensus had priced.

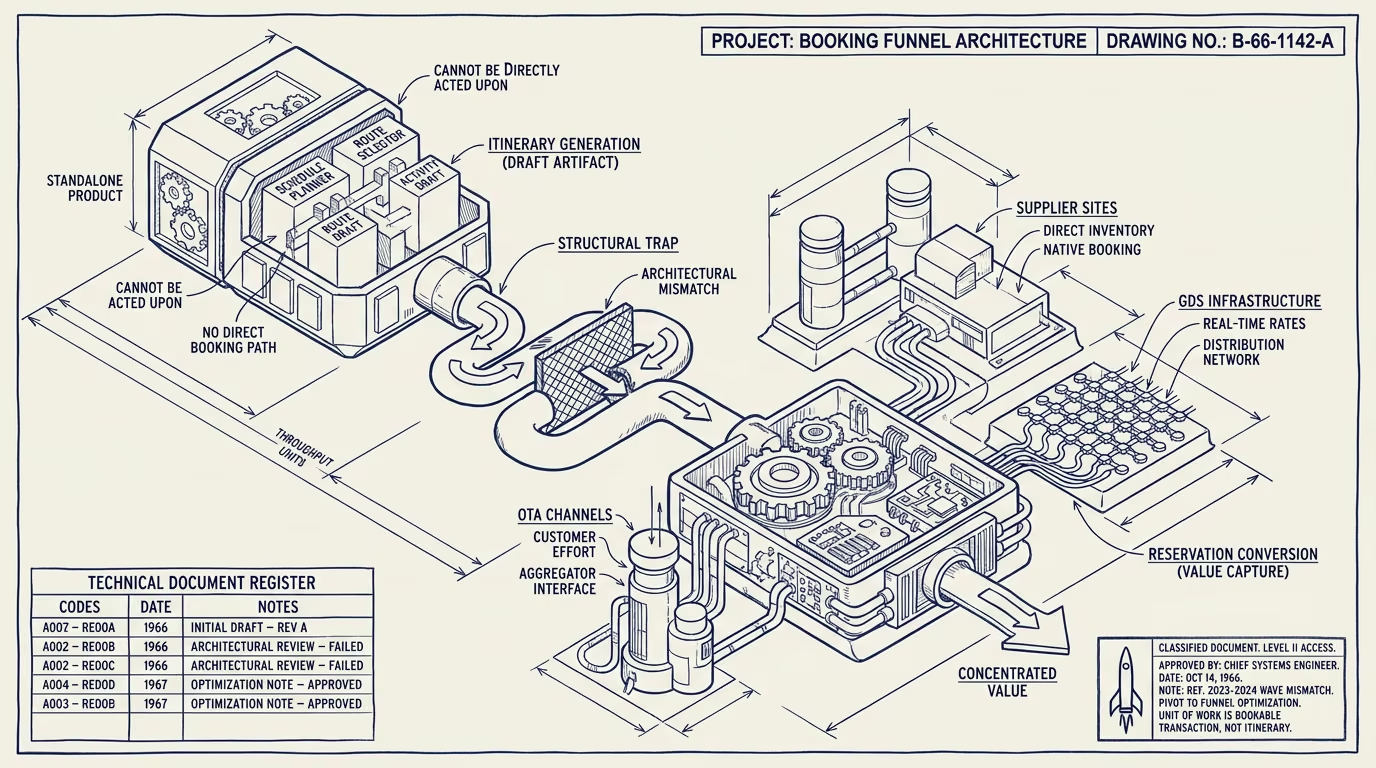

The structural reason was visible from the start to the operator class working in adjacent travel categories. Itinerary generation is the wrong unit of work for an AI agent because the customer's actual want is the bookable fulfillment, not the itinerary draft. The standalone itinerary-generation product produces an artifact (the itinerary) that the customer cannot directly act on; the customer still has to take the itinerary into the booking channels (the OTA, the supplier-direct site, the travel-agent, the GDS-mediated channel) and convert it into actual reservations. The booking conversion is where the customer's effort actually concentrates and where the value-capture is structurally available. The standalone itinerary-generator captures none of this, which is why the unit economics of the standalone-product category did not work.

Expedia's 10-K disclosure language through 2024-2025 confirms this read. The company's AI investment, as described in the public filings, has been concentrating on booking-funnel optimization, post-disruption rebooking workflows, and other deployments where the AI-generated artifact is the bookable-fulfillment rather than the standalone itinerary. The shift in the disclosure language is small and consistent across reporting cycles, signaling that the operational read at the company has aligned with the booking-funnel-as-product framing rather than the itinerary-as-product framing.

This piece walks the wave, the structural mismatch, the Expedia confirmation, and what the next category of AI-travel products needs to internalize.

What the wave looked like at peak

The 2023-2024 wave at peak produced a substantial cohort of products that took similar shape. The user provides a free-text trip request. The product produces a multi-day itinerary including hotel suggestions, restaurant suggestions, daily routing, and rough budgeting. The user reviews the itinerary, possibly iterates with the AI to refine specific elements, and ends up with a polished itinerary document the product can export to PDF, calendar, or shared link.

The products demonstrated genuine capability. The itineraries the systems produced were, on the median case, comparable in quality to what a human travel agent would produce for a similar request. The trade-press coverage was generous. The venture-class funding was substantial.

The products did not, on the median case, produce booking conversion. Users took the itineraries and went somewhere else to do the booking, with the somewhere-else being either the major OTAs (Booking, Expedia) or the supplier-direct sites (chain hotel reservation systems, airline direct booking). The standalone itinerary-product captured the planning effort and lost the booking effort, which is where the revenue concentrates in travel.

Why the unit of work was wrong

The structural mismatch ran along several dimensions.

The itinerary itself is a low-conviction artifact. The user does not, generally, fully trust an AI-generated itinerary without doing their own research-and-verification work on the recommended hotels, restaurants, and routing. The verification work happens before the booking, with the consequence that the user's effort and attention are concentrated at the verification phase, not at the AI-itinerary-generation phase. The product captures the wrong moment of the user's attention.

The booking infrastructure that converts an itinerary into reservations is itself substantial work. Hotel reservation systems, flight booking, restaurant reservation networks, and the activity-and-tour booking ecosystem each have their own integration requirements, payment flows, and confirmation infrastructure. The standalone-itinerary-product that does not include this layer cannot capture the booking, which means it cannot capture the revenue that the booking would have produced.

The customer's loyalty-and-account relationships sit at the major OTAs, the chains, and the airlines, not at the standalone-itinerary-product. The customer who has accumulated points-and-status at a particular OTA or chain is not going to migrate that relationship to the itinerary-product. The booking flows back to the established loyalty-relationship, which means the standalone-product is forever in a customer-acquisition-only position.

The combined effect is that the standalone-itinerary-product is structurally a planning-tool with no path to revenue capture. The unit economics do not work because the product is upstream of where the value is captured.

The Expedia confirmation

Expedia's 10-K disclosure language, in the filings through 2024 and into 2025, has shifted. The company's AI investment is described in terms of booking-funnel optimization, disruption-management, and workflow-automation rather than in terms of standalone itinerary-generation. The shift is consistent across reporting periods and is the kind of language change that signals the company's operational priorities have settled.

The implicit confirmation is that Expedia, with substantially better data than any of the standalone-itinerary-products on what actually drives travel-product revenue, has concluded that the booking-funnel optimization is where the AI investment produces returns, and the standalone-itinerary-generation is not. The structural read on the broader category should follow the Expedia read.

What the next category needs to internalize

For founders building AI-travel products in 2026 and beyond, the operator-class read is to build for the booking-funnel-and-fulfillment shape rather than the standalone-planning shape. The customer's value capture is at the booking; the product's value capture has to be at the same place.

Several specific shapes work. The booking-flow-optimization shape integrates AI into the existing booking funnel at the major OTA or supplier-direct sites, improving the discovery and conversion experience without requiring the user to leave the booking environment. The rebooking-and-disruption-management shape, discussed elsewhere, captures the agentic-AI capability against the well-fitted problem shape. The travel-agent-augmentation shape provides AI capability to professional travel agents in TMC and corporate-travel-management contexts, with the agents' existing customer relationships providing the value-capture infrastructure.

The shape that does not work is the standalone-AI-itinerary-product that produces an artifact the user cannot act on inside the product. The 2023-2024 wave built against this shape and the wave faded for the structural reason. Founders in 2026 building against the same shape will reproduce the wave's outcome.

The Expedia 10-K confirmed what the part that holds had implied from the start. The booking funnel is the unit of work that captures value. The itinerary draft is upstream of the unit of work. The next category of AI-travel products needs to build for the unit of work that captures value, and the operator-tier is increasingly able to recognize the difference. The wave is over. The operator lessons survive. Build for the funnel; the standalone planning is not the product.

—TJ