American picked the fight with the agencies. The agencies kept the routes.

TL;DR [show]

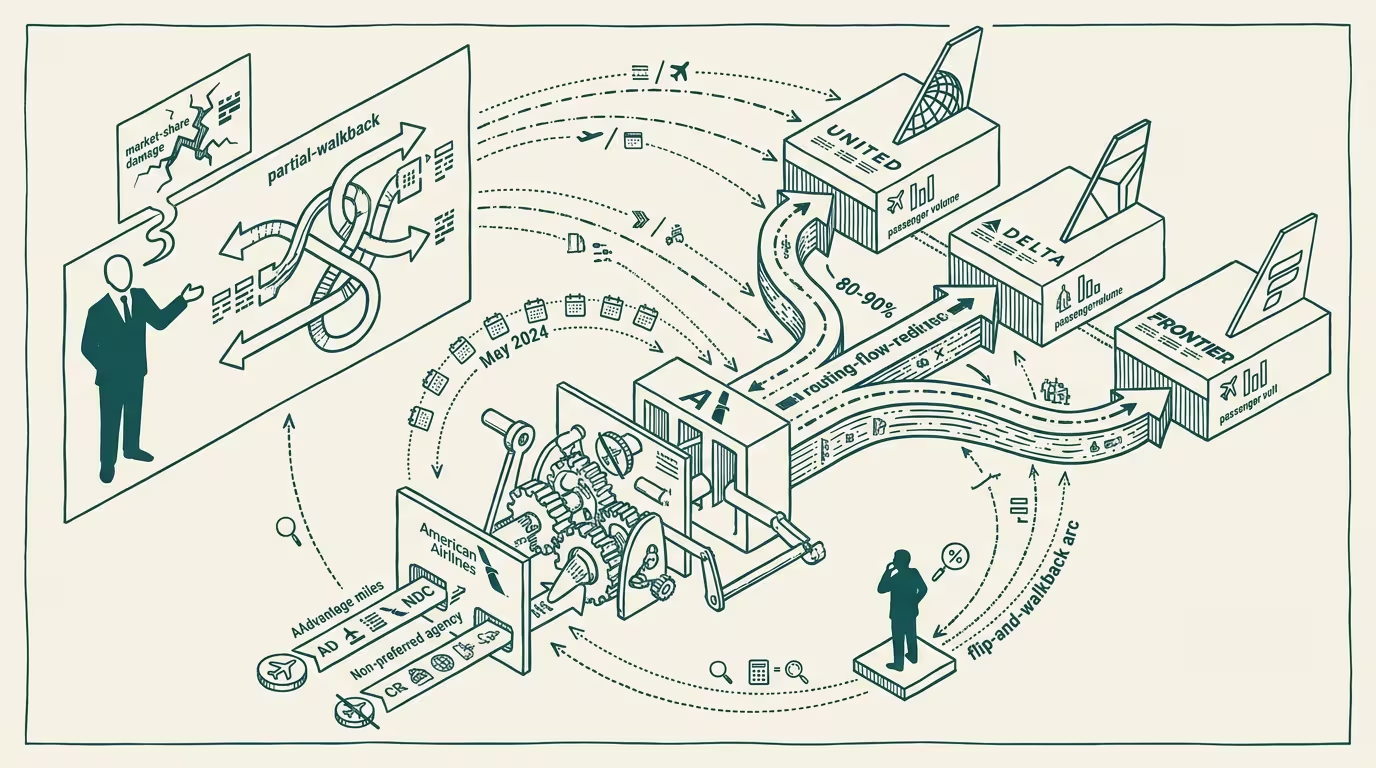

American's hard-line NDC strategy stripped AAdvantage miles from non-preferred-agency bookings starting May 2024; agencies flipped 80-90% of AA share to United/Delta/Frontier in response. Mid-year, CEO Isom acknowledged the market-share damage; the airline simultaneously rolled out AAdvantage Business as a direct-distribution end-run around the agencies it had just punished. The case study is in distribution-channel power.

In May 2024 American Airlines stopped awarding AAdvantage miles for tickets booked through travel agencies that were not on the airline's preferred-NDC-distribution list. The argument, internally, was that NDC adoption had been slow and the airline needed leverage to force the migration. The argument made sense in the conference room. Outside the conference room, the agencies that had been doing $40 billion of annual U.S. corporate-travel booking volume read the move as a direct attack and responded the way attacked partners respond.

Within ninety days agencies had moved 80-90% of their AA share to United, Delta, and Frontier. The flip was, by every measure available, the largest market-share movement in U.S. domestic-travel-distribution in a decade. American had assumed agencies would absorb the punishment because they had to. The agencies had assumed otherwise.

Mid-year, AA CEO Robert Isom acknowledged the market-share damage in a public statement. The airline did not reverse the NDC policy. The airline did, on the same calendar, roll out AAdvantage Business: a direct-distribution-to-corporate-buyer offering that bypassed the agency layer entirely while letting the corporate buyer earn AAdvantage credit on direct-booked travel. The two moves together were the airline trying to do an end-run around the agencies through the loyalty layer after it had punished them through the NDC layer.

The structural question is whether the AAdvantage Business gambit recoups the AA-share loss to United and Delta.

The early read is mixed. AAdvantage Business has reasonable initial uptake among the smallest end of the corporate-travel market, where the buyer was already doing a fair amount of direct-booking and the AAdvantage credit is a marginal reward worth the simpler workflow. The mid-market and enterprise corporate buyers have, on the available evidence, not switched. They were already heavy users of agency-managed travel programs; the agency relationship handled policy compliance, expense reconciliation, and disrupted-trip support that AAdvantage Business does not offer. The agency relationship was sticky for the right reasons, and a frequent-flyer-program-credit benefit alone was not enough to break it.

The pattern that worked at the small end did not scale to the large end. The pattern that scaled at the large end was the pattern American was punishing. The airline ended up with both halves of the market harder to serve than it had been before the policy.

Three operator-class lessons from this case study.

First, distribution-channel power is structurally underestimated by the operator who controls the product. American assumed that because it controlled the airline seats, it controlled the value chain. The agencies controlled the customer relationship, the policy-enforcement workflow, the expense-reconciliation integration, and the disrupted-trip-support apparatus. Those four things were the value-add the agency provided, and the agency provided them on top of every airline's seat inventory equally. Punishing one carrier's bookings cost the agency some preferred-customer status with that carrier; switching to United or Delta cost the agency nothing. The agency's leverage was the customer relationship, and American did not have a substitute.

Second, the loyalty-layer end-run is structurally too narrow to replace the agency-layer relationship. AAdvantage Business is, in the corporate-travel-buyer's frame, a credit-card-equivalent benefit. Credit-card-equivalent benefits do not replace workflow infrastructure. The corporate-travel-buyer who would have switched to AAdvantage Business is the buyer who was not using a TMC anyway, which is to say a small fraction of the addressable market. The buyer who is using a TMC is buying a workflow product, and the workflow product is, in 2024, what American did not have.

Third, the operator who picks a multi-quarter fight with their distribution layer needs to have built the alternative distribution layer first. American built AAdvantage Business in parallel with the NDC fight, but the timeline of building a new distribution channel is materially longer than the timeline of breaking the existing one. The agencies adapted in ninety days. AAdvantage Business needs three to five years to scale to a meaningful fraction of corporate-travel volume. In the gap, the airline absorbs the share loss. The airline has, in 2024, no acceptable way to backfill the gap.

The thing that crosses pillars is that distribution-channel-power dynamics recur across categories. The airline-vs-agency case is structurally analogous to the SaaS-vendor-vs-channel-partner case, the consumer-product-vs-retailer case, the streaming-platform-vs-cable-bundle case. In every one, the operator who controls the product underestimates the channel partner's leverage, picks a fight to capture more margin, and discovers in the medium term that the channel partner had options the operator did not anticipate. The pattern is decades old. American's NDC fight is the 2024 version of it.

The honest summary is that American picked a fight with the agencies, the agencies kept the routes, and the airline is now operating a distribution strategy that captures less of the corporate-travel category than it captured in 2023. The AAdvantage Business gambit was structurally necessary as a hedge, but the hedge does not replace the loss. The airline's CEO acknowledged the damage. The damage continues.

The part that holds for any operator-against-channel decision is to map the channel partner's substitutes before initiating the fight. American mapped the agencies as having no substitutes. The agencies had United and Delta. The map was wrong. The cost of the wrong map is, of course, paid by AA shareholders for the next several quarters, by AA's corporate-travel sales team trying to win back the share, and eventually by the AAdvantage Business roadmap that has to absorb the gap the NDC fight created.

—TJ