Hotels printed margin. Airlines printed apologies.

TL;DR [show]

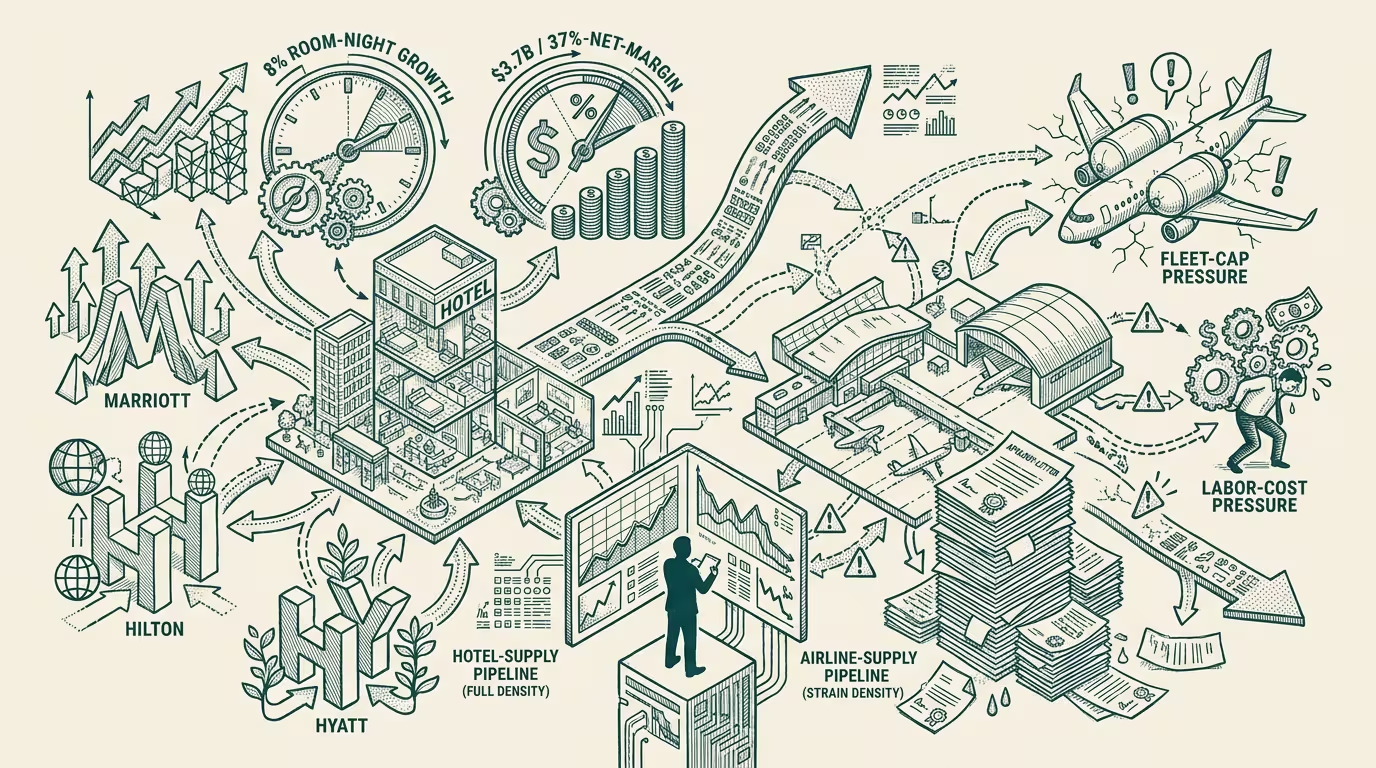

Q3 2025 results: Booking Q3 8% room-night growth, Airbnb $3.7B revenue at 37% net margin, vs. airlines bleeding through fleet-cap and labor pressure. Operator read: the divergence is structural — hotels run a less commoditized supply graph than airlines, and the agentic layer struggles harder there; the OTA-vs-airline asset-light arbitrage is now in its third compounding year.

Q3 2025 reporting closed with a structural divergence the trade press wrote up category by category and the operator class should be reading at the cross-category layer.

Hotels: Booking reported 8% room-night growth in Q3. Airbnb posted $3.7B revenue at 37% net margin. Marriott, Hilton, and Hyatt all reported margin expansion year-over-year. The hotel category was operating-strong on every relevant metric.

Airlines: every U.S. major absorbed cost pressure through fleet-cap constraints (Boeing 737 MAX delivery delays, A321XLR fleet-induction friction), labor-cost increases (the post-Air-Canada-strike wave hitting U.S. carriers), and IRROPS-class disruption. United, Delta, American, and Southwest all reported margin compression year-over-year. The airline category was operating-stressed on every relevant metric.

_Hotels print margin. Airlines print apologies._ Hold the divergence in view. Everything that follows traces back to it. The divergence is structural and is now in its third compounding year.

Trace it back to supply-graph commoditization and one variable surfaces. A hotel room in a specific market is differentiated from another hotel room in the same market by amenity bundle, brand position, and operating reputation. A flight in a specific market is, in operating terms, mostly fungible across carriers (with marginal differentiation on schedule, loyalty status, and product class). The supply-graph differentiation gives hotels pricing power that airlines do not have. The agentic layer that compresses pricing power compresses airline pricing faster than hotel pricing, because the airline's pricing-power floor was already lower.

Trace it back to asset-light-vs-asset-heavy economics and a second variable surfaces. Booking and Airbnb hold no inventory, no aircraft, no labor unions, no fleet-cap exposure, no IRROPS-class disruption cost. They run pure-platform economics. The asset-heavy operators (airlines, vertically-integrated hotel operators) absorb the operating cost; the asset-light platforms capture the margin. The arbitrage has been visible since 2022 and continues to compound. By Q3 2025 the cumulative asset-light advantage was three full reporting cycles deep, with no visible inflection.

Trace it back to agentic-AI exposure and a third variable surfaces. AI agents producing travel-planning recommendations have an easier time substituting carriers (because the underlying product is more commoditized) than substituting hotels (because the underlying product is more differentiated). The agentic-layer effect on airline pricing pressure is therefore stronger than the agentic-layer effect on hotel pricing pressure. By 2026-2027, the differential exposure is going to be more visible, not less.

What's the thing that crosses pillars? Asset-light-vs-asset-heavy and commoditized-supply-vs-differentiated-supply are the two structural variables that decide which travel-category captures rents in the agentic-AI cycle. Hotels run on the favorable side of both. Airlines run on the unfavorable side of both. OTAs run on the favorable side of asset-light and ride the discovery-layer-inversion question separately.

What survives all of this is that Q3 2025 is one of the cleaner cross-category data points for the structural divergence, the divergence is durable through at least the 2027 reporting cycle, and the part that holds is to position any travel-category investment thesis with explicit treatment of which side of the two structural variables the company sits on. Most investment theses are not running that explicit treatment. The ones that are are repricing airline equity downward and asset-light-platform equity sideways or upward.

Hotels printed margin. Airlines printed apologies. The divergence is, in operating terms, the leading indicator for the next three reporting cycles. The trade press will, of course, continue to write each category's earnings in isolation. The cross-category pattern is the durable read that matters.

—TJ