Urgency-led conversion is a leading indicator. The retention haircut is the trailing one.

TL;DR [show]

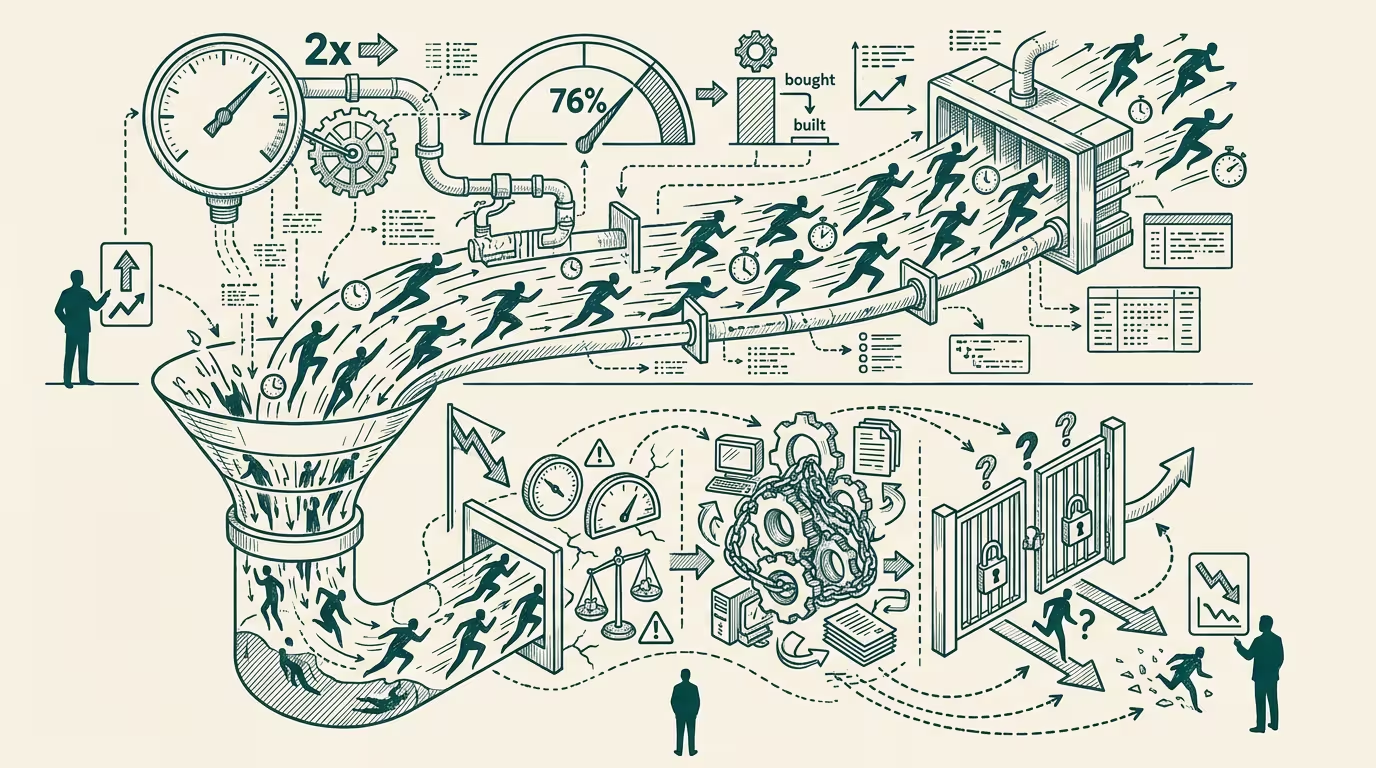

Menlo Ventures' 2025 enterprise AI report: 76% of AI use cases now purchased vs. built (up from 53% in 2024), and AI deal conversion runs at 2x traditional SaaS. The 2x advantage reflects buyer urgency from competitive pressure, not measured IT evaluation, meaning the fast-adopter cohort is also the fastest-to-swap cohort when the next capability generation arrives. AI SaaS retention assumptions need a haircut.

Menlo Ventures published its 2025 enterprise AI report in early Q4. Two numbers landed as headlines. 76% of AI use cases are now purchased rather than built (up from 53% in 2024). AI deal conversion runs at 2x traditional SaaS conversion rates. The trade press read the combination as evidence of healthy enterprise-AI adoption.

What's actually happening underneath the headline?

_Urgency-led conversion is a leading indicator. The retention haircut is the trailing one._

The 2x conversion advantage doesn't reflect measured IT evaluation. It reflects competitive-pressure-driven buyer urgency. CIOs in 2025 are buying AI tools because their peers are buying AI tools and the board is asking why the company doesn't have an AI strategy. The buying decision is partially performative, partially defensive, partially genuine — but the fraction driven by urgency is structurally larger than the fraction driven by measured technology fit.

Why does that matter for retention? Because the fast-adopter cohort is also the fastest-to-swap cohort. A buyer who purchased an AI tool in 2025 under competitive-pressure urgency is a buyer who will swap to a different AI tool in 2026 under the same urgency, when the next capability generation arrives. The buying decision was speed-driven, not fit-driven. Speed-driven decisions don't carry the integration depth or workflow embedding that drives traditional-SaaS retention. AI-SaaS retention assumptions calibrated to traditional-SaaS retention curves are operating-stale.

When does the haircut surface? In the 2026-2027 cohort metrics, not in the 2025 conversion metrics. Right now the conversion numbers look healthy because the urgency is producing closes. The retention metrics for the 2025 cohort won't be visible until 2026-2027 when the renewal cycles hit. Operators reading the conversion numbers should be modeling retention discount factors of 30-50% relative to traditional-SaaS retention assumptions through the next two renewal cycles. The discount factor will moderate as the urgency wave passes and selection-on-fit reasserts; until then, retention is structurally weaker than the headline conversion numbers suggest.

What differentiates AI-SaaS operators inside this cohort? Integration depth, not capability differentiation. AI capability is converging across the frontier-model providers; AI SaaS products built on top of those models are differentiating less on capability than on integration. The vendors with deep workflow integration, durable data-engineering positions, and high switching costs at the integration layer are the vendors whose retention curves survive the urgency-cohort cycling. The vendors selling on capability differentiation alone are the vendors whose 2027 retention numbers reveal the haircut.

The same shape recurs in any category where buying decisions are driven by competitive-pressure timing rather than measured fit. AI-SaaS in 2025-2026. Healthcare-tech in COVID-era 2020-2021 (rapid telehealth adoption with high churn through 2022-2023). FinTech-payments in early-2010s deployment cycles. Each category has the same structural shape: urgency-conversion is a leading indicator that retention discount needs to apply.

What survives all of this is that the 76% / 2x metrics are real and conversion-positive, the retention curve calibrated to those metrics is operating-thin, and the discipline for AI-SaaS founders is to build integration depth ahead of urgency-driven conversion volume rather than chasing the volume directly. Operators who build for retention durability are positioned for the post-urgency-wave market. Operators who optimize for the headline conversion are positioned for the cohort-cycling that follows.

Urgency-led conversion is a leading indicator. The retention haircut is the trailing one. Enterprise AI is a market where the leading-trailing gap is operationally visible. Operators who price the gap into their planning are operating-coherent. Operators who price the conversion as durable are pricing against a structural reality the renewal cycles will eventually surface.

—TJ