The Trump election reset the US AI regulatory calendar. Canadian operators should not breathe easy.

TL;DR [show]

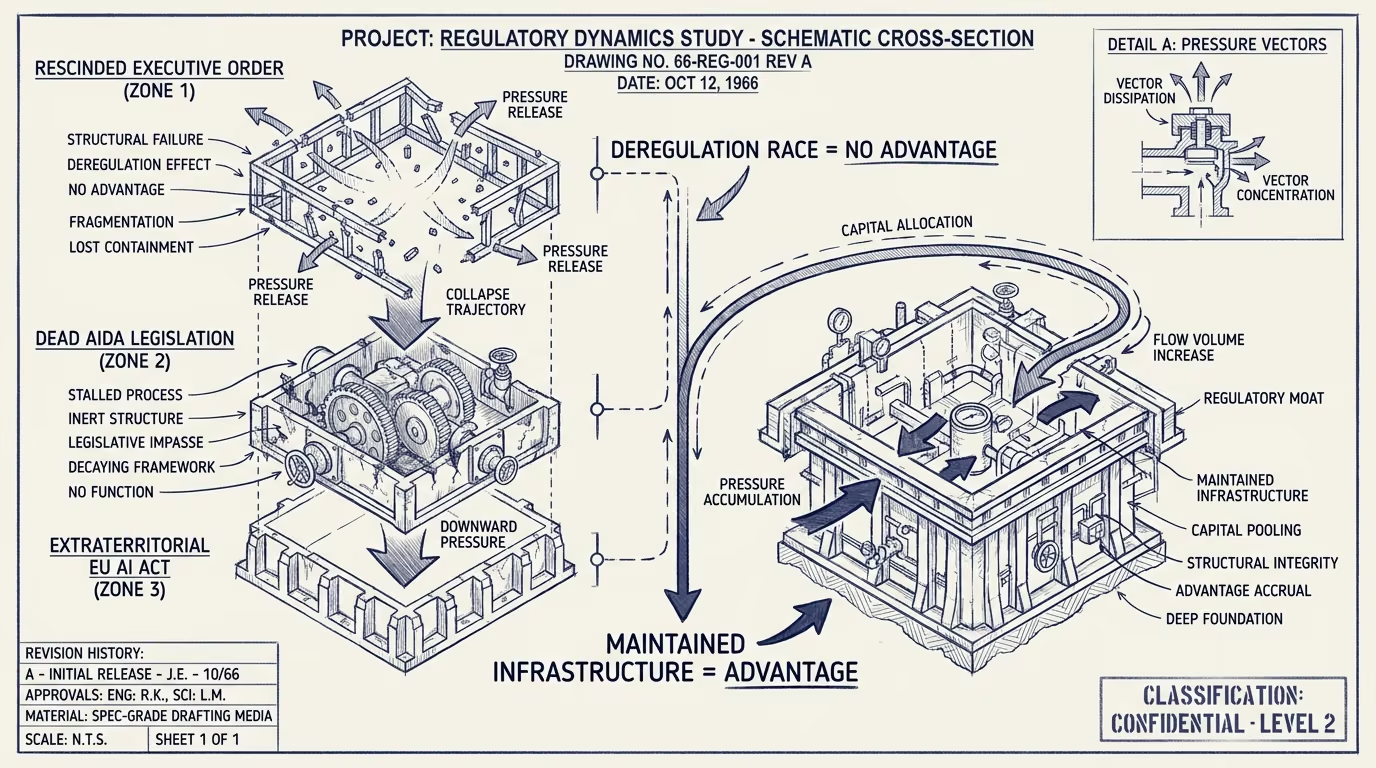

Trump's November 2024 election signals U.S. federal AI deregulation through the next four years, with the Biden-era executive order likely to be rescinded early in the new administration. The Canadian read on the U.S. shift is more complicated than the surface reading implies. AIDA is already dead in the Canadian legislative session. The EU AI Act applies extraterritorially to Canadian companies serving EU customers. The U.S. deregulatory signal pulls international AI capital allocation toward U.S.-domiciled companies, with the consequence that Canadian operators face structural pressure that the headline regulatory shift does not directly produce.

The November 2024 U.S. presidential election produced the political environment for federal AI deregulation through the next four years, with the Biden-era executive order on AI likely to be rescinded early in the new administration and the broader regulatory posture shifting toward lighter-touch federal engagement. The U.S. shift has been broadly read as good-news for the U.S.-domiciled AI category and as either neutral or also-good-news for international AI operators.

The Canadian read on the U.S. shift is more complicated than the surface reading implies, and Canadian operators should not be reading the U.S. deregulatory signal as good-news for their own operating environment.

Several specific dynamics produce structural pressure on Canadian AI operators that the U.S. headline regulatory shift does not directly produce.

The first is that AIDA, Canada's primary AI regulatory legislation, is already dead in the current legislative session. The federal-level Canadian regulatory environment for AI is structurally weaker than the U.S. environment was even before the deregulatory shift, with the consequence that the U.S.-deregulatory move does not produce a relative-advantage for Canadian operators. The two environments are converging toward similar light-touch postures, but the U.S. version retains substantial state-level regulatory infrastructure (Washington's MHMDA, Illinois's WOPR-class legislation, California's various AI bills, the broader patchwork) that Canadian operators do not benefit from.

The second is that the EU AI Act applies extraterritorially to Canadian companies serving EU customers. The Canadian operator reaching EU customers must meet the EU compliance bar regardless of the U.S. or Canadian regulatory posture. The U.S. deregulatory shift does not affect this constraint. Canadian operators continue to face the EU compliance burden as the binding constraint on international expansion.

The third is the capital-flow dynamic. The U.S. deregulatory signal pulls international AI capital allocation toward U.S.-domiciled companies. International investors evaluating AI investments now face an environment where the U.S. regulatory environment is the lightest among major markets, the U.S. capital-availability is the deepest, and the U.S. talent-availability is the strongest. The combination produces structural capital-allocation pressure that pulls investment away from Canadian-domiciled companies and toward U.S.-domiciled companies, even when the underlying technology and market opportunity is similar.

For Canadian AI operators reading the post-election environment, the practical advice is to position the company against the international-capital-flow dynamic rather than against a domestic-deregulation expectation. Several specific moves help. Establishing U.S. operating presence (subsidiary, sales office, executive-tier presence) helps with the capital-allocation question. Maintaining EU compliance posture helps with the European market access. Engaging with the Canadian provincial-and-federal regulatory environment helps with the domestic policy advocacy work that should be pushing for the AIDA-equivalent reintroduction.

For Canadian investors evaluating AI investments, the read is that the relative-position of Canadian AI companies has shifted unfavorably relative to U.S. peers, with the consequence that valuation discounts may persist longer than the previous cycle suggested.

The Trump election produced the U.S. deregulatory shift. The Canadian part that holds is not that the shift is good news. The shift is structurally pressure on Canadian-domiciled AI operations through capital-flow, talent-flow, and competitive-positioning dynamics that the headline regulatory shift does not directly produce. Canadian operators reading the headline as relief should be reading the structural dynamics as pressure. Build accordingly.

—TJ