The labs filed to become utilities

TL;DR [show]

In a single week the AI labs revealed how the compute-and-energy buildout gets paid for: Anthropic filed confidentially for a roughly $965B IPO, OpenAI followed days later into a reported $3.6 trillion IPO pipeline, and Apollo led a $35 billion private-credit vehicle for more than 20 gigawatts of Broadcom compute through 2028. The piece argues the financing structure, not the valuations, is the signal: an asset-backed, leveraged, long-offtake instrument is how you finance a fleet of power plants, and the IPO is its equity tranche. Financed like a utility, a lab gets governed like one, which is why its best model just left the consumer subscription. The financing coda of the energy-sovereignty arc, two floors down from the nation and one floor down from the lab.

Twice now I have written that the binding constraint on artificial intelligence is energy. First at the scale of a country, arguing there is no AI sovereignty without energy sovereignty. Then at the scale of a lab, when Anthropic started paying a rival more than a billion dollars a month to rent a data center it could not build fast enough. Both times I left a question on the table without quite naming it. If the buildout is this big, and the constraint is this physical, who actually pays for it.

This month they told us. The public markets, and Wall Street's private-credit desks.

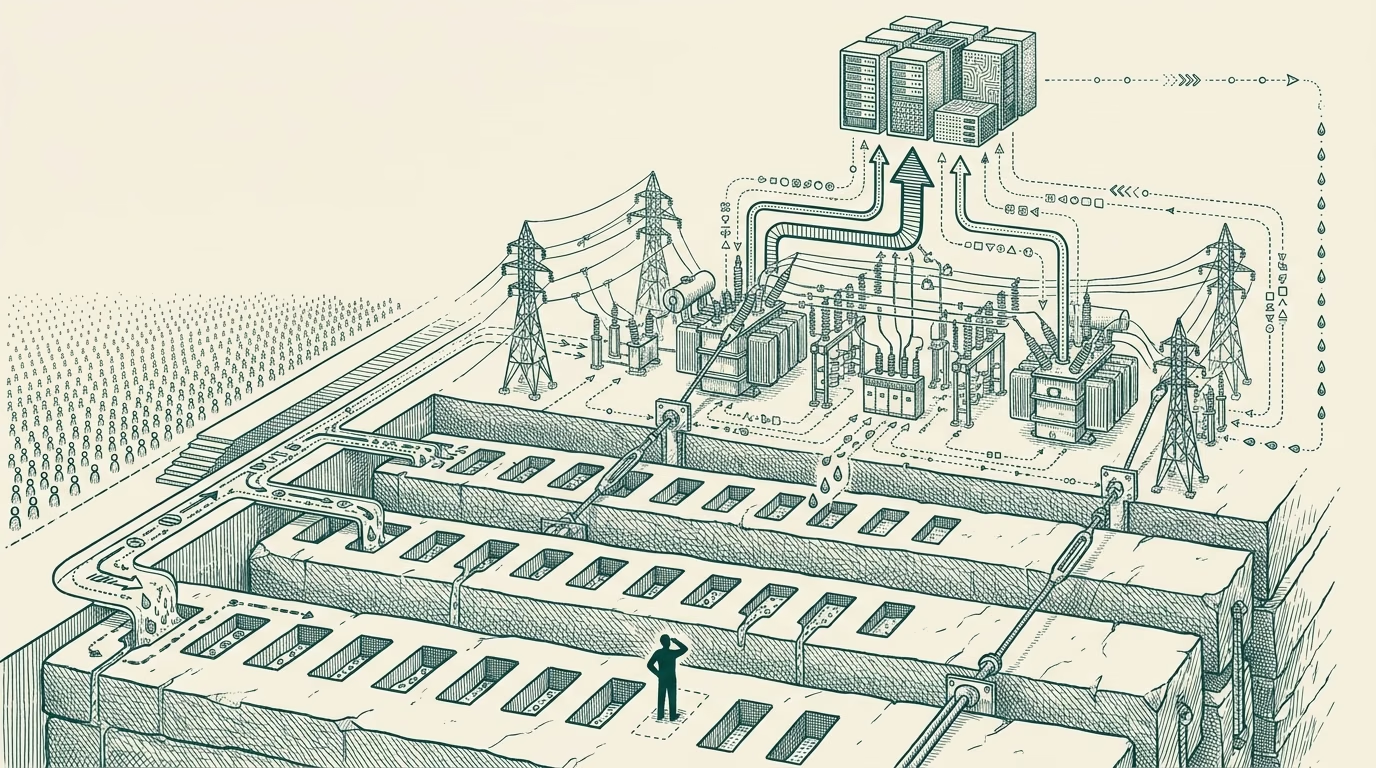

Look at the week. Anthropic filed confidentially for an IPO at a reported nine hundred sixty-five billion dollars. OpenAI filed days later, into what Bloomberg now calls a three-and-a-half-trillion-dollar pipeline of AI listings stacking up for the back half of the year. And in the same window Apollo led a thirty-five-billion-dollar capital solution for Broadcom, with Blackstone and a syndicate of banks behind it, targeting more than twenty gigawatts of compute through 2028. Read those three events as valuations and you get the obvious story, the one every outlet ran: the AI boom is cashing in, the window is hot, the money is chasing the winner. Read them as a financing structure and you get a different story, and the different one is true.

Start with the Apollo vehicle, because it is the most honest about what it is. Thirty-five billion dollars, asset-backed, bundling the chips and the networking and the power and the long-term customer commitments into a single instrument that the credit markets can underwrite. That is not how you finance a software company. Software companies raise equity and burn it on people. That is how you finance a fleet of power plants. Long-lived physical assets, leveraged against contracted future cash flows, sold to bondholders who want a coupon and a maturity date and do not especially care what runs on top. Twenty gigawatts is not a metaphor. It is roughly the output of twenty large nuclear reactors, and somebody is structuring debt against it the way you structure debt against generation capacity, because functionally that is what it now is.

The IPOs are the equity tranche of the same conversion. You do not file to go public at the moment your unit economics close. You file when the capital you need has outgrown what private rounds and your own balance sheet can supply, and the only pool deep enough to fund the next leg is the public market. Anthropic and OpenAI are not going public because the business is finished. They are going public because the power plant is not, and the power plant is expensive, and the patient money has run out before the buildout has.

I want to take the bull case seriously, because it is not stupid. The demand is real. The revenue curves are real, OpenAI was reportedly clearing around two billion dollars a month earlier this year, and you do not manufacture a three-trillion-dollar listing pipeline out of nothing. A reasonable person looks at these filings and sees the most important technology of the era finally large enough to belong in everyone's index fund, and that person is not wrong about the importance. But importance is not the tell. The tell is in the shape of the paper. OpenAI is reportedly losing something like a dollar twenty-two for every dollar it earns, and filing anyway, at a valuation north of eight hundred billion. That is not a company harvesting a mature business. That is a company betting that the public markets will fund the moat before the economics close, and going to those markets precisely because no one else can write a check that big.

Here is what changes when you finance research like a utility. You get governed like one.

Patient capital tolerates a decade of loss in exchange for a shot at owning the future. Bondholders do not. Public shareholders do not. The moment your twenty gigawatts sits inside a leveraged, asset-backed vehicle with utilization assumptions baked into the debt covenants, the people holding that paper need the capacity used, and used at a price that services the loan. Frontier research stops being governed like research and starts being governed like a power company's capital plan, where the binding question every quarter is not what is the most interesting thing we could build, but what keeps the substation paid. The financing structure becomes the strategy. It always does, the moment the financing structure is this large and this leveraged.

And this is where the two stories I have been telling this month close into one circle, because the same pressure that sends a lab to the bond market is the pressure that just took its best model out of my subscription. Two days ago I wrote about Anthropic pulling Fable out of the consumer plans and metering it by the token. At the time I read it as a cost-structure decision, which it is. But it is the same decision as the IPO, seen from a different floor. A research lab can give the frontier away to delight its users. A utility under debt service cannot. It has to meter the expensive thing to whoever clears the cost, which means the API and the enterprise contract, and it has to stop handing it to the flat-rate consumer at a loss, because the flat-rate consumer does not service the bond. The filing and the meter are the same act of capital discipline. One faces Wall Street. The other faces me. They were written by the same arithmetic.

The boring layer keeps turning out to be the real one. In cloud it was the data center under the software. In mobile it was the app-store toll under the app. In this cycle it is the megawatt under the model, and now, one floor further down, it is the financing under the megawatt. We spent three years arguing about which lab had the best model. The labs just answered, with a trillion dollars of filings and a thirty-five-billion-dollar bond against twenty gigawatts, that the model was never the asset. The capacity is the asset. The model is the thing you run to justify the capacity, and the financing is the thing that decides whether you get to keep running it.

So the competitive set is quietly narrowing in front of us, and it is narrowing along a line that has almost nothing to do with intelligence. The question stops being who has the smartest model and becomes who can underwrite twenty gigawatts for a decade without the cost of capital eating them alive. That is not a question software companies are built to answer. It is a question utilities answer, and states answer, and the handful of integrated giants with their own balance sheets and their own power strategies can answer. The labs that cannot are going to the public markets to borrow the answer, and the terms of that loan will shape what they are allowed to build long after the launch-day benchmarks are forgotten.

I closed the country piece by saying six million roofs is the first stone, and the lab piece by saying the model is downstream of the power. I will close this one a floor lower still. This was the month the power got a coupon and a maturity date, and the labs signed for it, and somewhere in the fine print of those filings is the real roadmap, the one that outranks anything they will say on stage. Not the model they want to build. The debt they have to service to build it.

—TJ